Swiss mortgage interest rate forecast

Our assessment of the mortgage market

How will mortgage interest rates develop over the coming months? Find out how our experts view developments on the mortgage and real estate markets.

Status as at: 18.6.2026

Editorial deadline: 18.6.2026

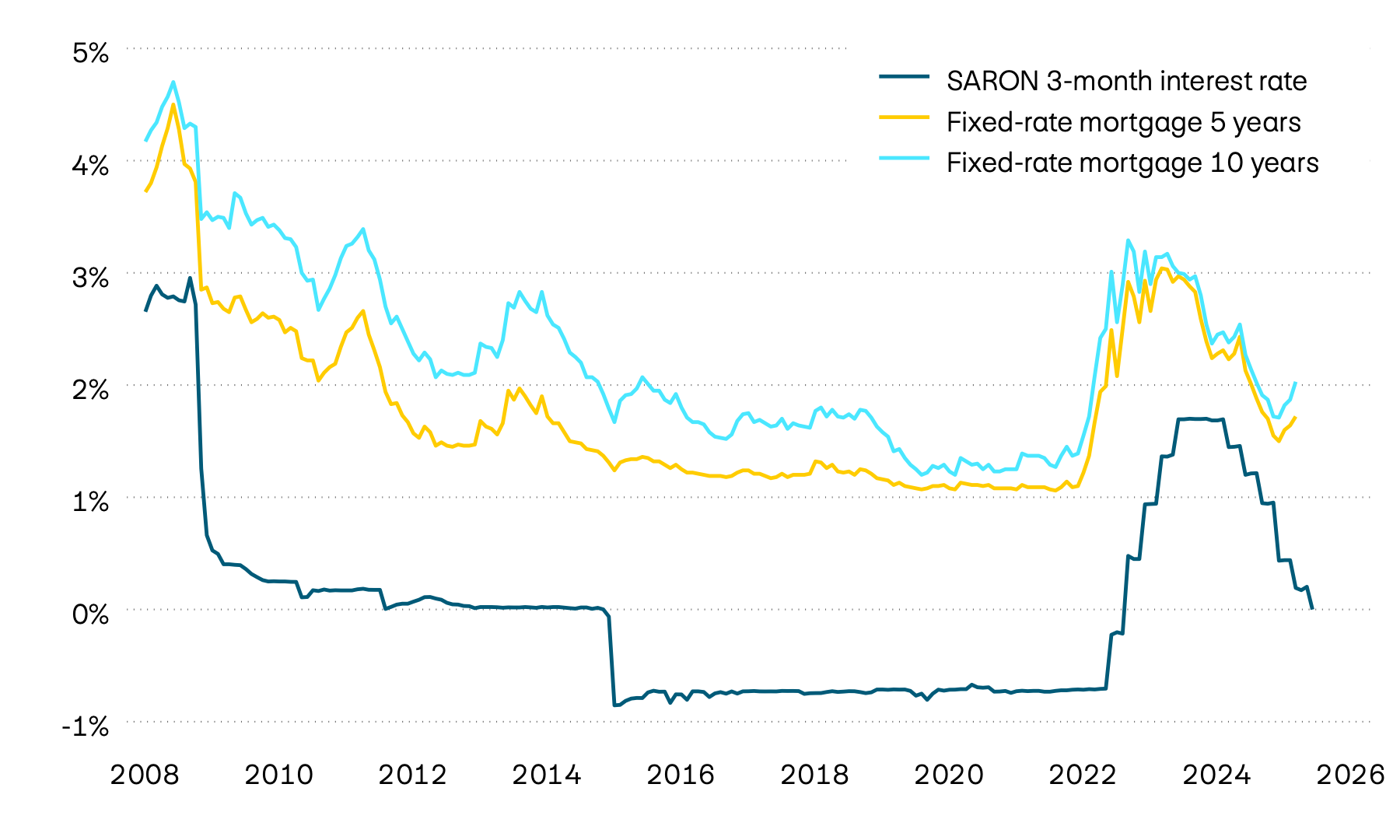

- The Swiss National Bank (SNB) is maintaining its zero interest rate for the time being. In the medium term, however, it could return to a positive policy rate in light of the improving economic outlook and the international monetary policy environment.

- That said, Saron mortgages remain very attractive.

- Fixed-rate mortgages also offer attractive conditions thanks to low capital market interest rates .

Current economic situation in Switzerland

After a difficult second half of 2025, the Swiss economy stabilized at the start of 2026, growing by 0.7 percent in the first quarter thanks to a moderate recovery in the industrial sector. Business sentiment has also improved in recent months, underscoring these recovery trends.

Our interest rate forecast at a glance

| Forecast for | 3 months | 6 months | 12 months |

|---|---|---|---|

| Forecast for Saron |

3 months |

6 months |

12 months |

| Forecast for 5-year fixed-rate mortgae |

3 months |

6 months |

12 months |

| Forecast for 7-year fixed-rate mortgage |

3 months |

6 months |

12 months |

| Forecast for 10-year fixed-rate mortgage |

3 months |

6 months |

12 months |

By international comparison, Switzerland remains one of the few currency areas with moderate inflation , which is why the SNB, unlike other major central banks, is not obliged to raise interest rates. As a result, the policy rate is likely to remain unchanged in the short term. In the medium term, however, this will give the SNB the flexibility to break away from the zero interest rate mark without reducing the interest differential to the major currency areas. Moderate rises in inflation are also likely to lead to a slight rise in capital market interest rates over the coming months, which is why fixed-rate mortgage interest rates are also likely to edge up gradually.

Just over three years ago, mortgage interest rates in Switzerland were still well above the current level and briefly exceeded the 3 percent mark. This was triggered by the Swiss National Bank’s (SNB) monetary policy with higher interest rates, which pushed its policy rate up to 1.75 percent due to high inflation after the coronavirus pandemic. Once inflation rates had fallen steadily again, the SNB gradually eased its monetary policy. This led to noticeably lower mortgage rates, even though they have not fallen to the same extent since the end of 2024, despite further policy rate cuts.

With the recent rise in inflation rates, major central banks worldwide are likely to adopt a more restrictive monetary policy again. This also gives the SNB leeway to move away from zero interest rates. However, we don’t expect it to take this step at the next monetary policy assessment on 24 September 2026, but only in spring 2027. With mortgage interest rates, on the other hand, we expect capital market interest rates to react earlier to moderately higher inflation in Switzerland and to rise slightly accordingly. Further interest rate developments therefore remain a key factor for mortgage interest rates in Switzerland.

In percent

Single-family homes and condominiums

Prices for owner-occupied apartments rose again in the first quarter of 2026, albeit less sharply than during the previous quarter. By contrast, the prices of single-family homes fell compared to the previous quarter, after having previously stagnated. The last time prices of single-family homes fell was in the fourth quarter of 2024. In addition to the currently high prices of single-family homes, which makes owner-occupied apartments a more affordable alternative for many prospective buyers, the persistently subdued consumer confidence and weaker economy are also expected to have an impact. In contrast, price dynamics are once again subdued for rental apartments. The reduction in the reference interest rate in September 2025 is increasingly being felt here. Its effects will only become visible in asking rents and existing rents with a time lag due to contractual adjustment periods.

Price index, January 2000 = 100

Interested in real estate as an investment opportunity? In our Investment compass under “Market overview”, you will find an analysis of the current situation on the Swiss real estate market.

What our experts say

“While prices for owner-occupied apartments rose again in the first quarter of 2026, the prices of single-family homes fell slightly compared to the previous quarter. We expect a moderate rise in interest rates on fixed-rate mortgages.“

Receive our assessment directly by e-mail after each SNB decision.

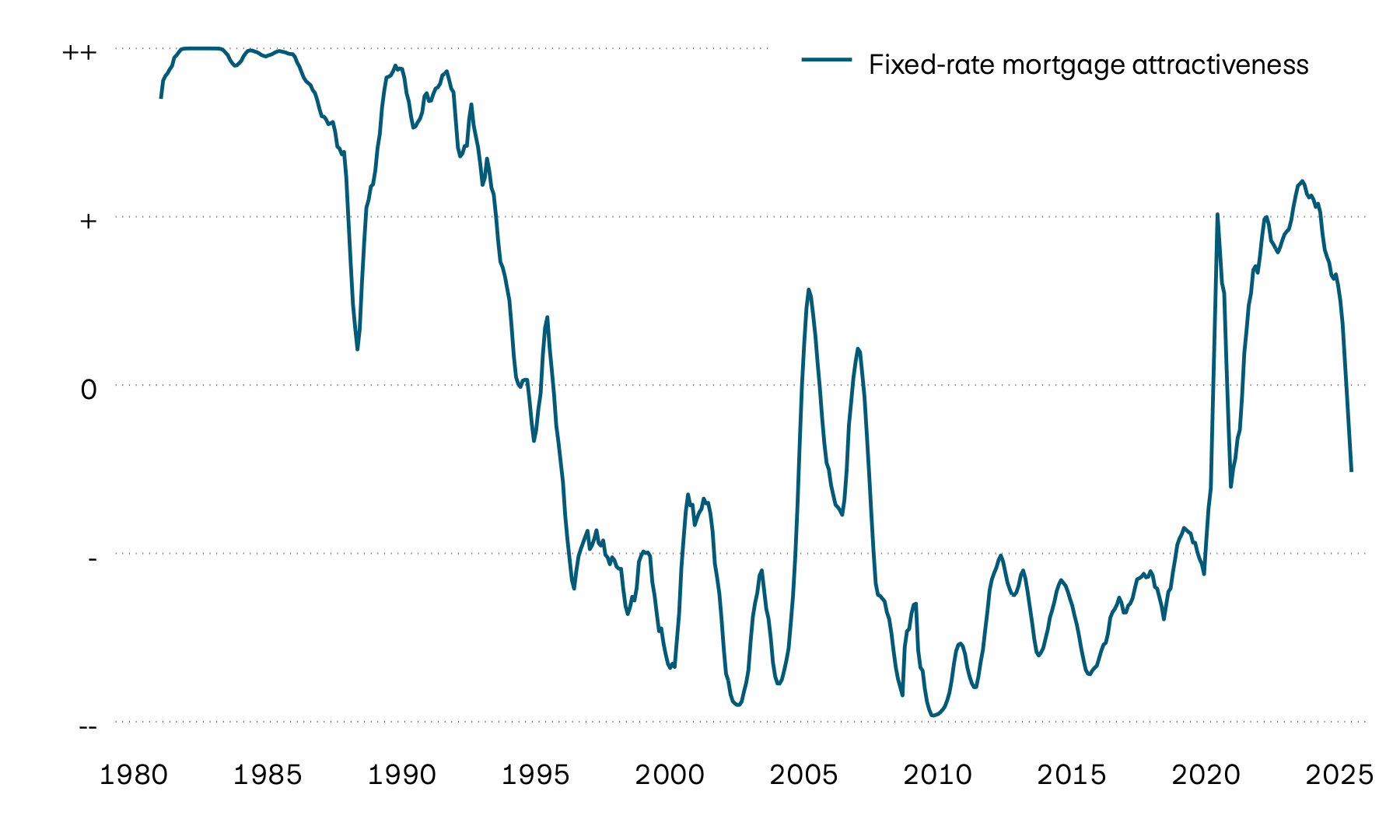

Fixed-rate mortgage or Saron mortgage?

Content Carousel

1

/

3

Which is the right mortgage for me?

Gain an overview of the conditions for the fixed-rate mortgage and the Saron mortgage with our mortgage comparison.

| Indicators | Q3 2025 | Q4 2025 | Q1 2026 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|---|

| Indicators GDP growth |

Q3 2025 0,7% |

Q4 2025 1,0% |

Q1 2026 0,5% |

2024 1,3% |

2025 1,0% |

2026 1,0% |

| Indicators Inflation |

Q3 2025 0,2% |

Q4 2025 0,0% |

Q1 2026 0,2% |

2024 1,1% |

2025 0,2% |

2026 0,6% |

| Indicators Unemployment |

Q3 2025 2,8% |

Q4 2025 3,0% |

Q1 2026 3,2% |

2024 2,5% |

2025 2,8% |

2026 3,2% |

| Indicators Net immigration |

Q3 2025 17‘000 |

Q4 2025 27‘000 |

Q1 2026 21‘000 |

2024 83‘000 |

2025 75‘000 |

2026 70‘000 |

| Indicators EUR/CHF exchange rate |

Q3 2025 0,94 |

Q4 2025 0,93 |

Q1 2026 0,90 |

2024 0,95 |

2025 0,94 |

2026 0,90 |

Source: Bloomberg, Allfunds Tech Solutions, BfS

-

Forecasting is a well-founded assessment, not a certainty. Whether now is the right time for you very much depends on your personal risk appetite, your financial situation and your individual needs.

If interest rates are falling: if you expect interest rates to continue to fall, a Saron mortgage may be an attractive option to benefit from the cuts, depending on the interest rate level.

If interest rates are rising: if you are expecting an interest rate rise or budget security is very important for you, it may be a good idea to fix the conditions over the long term with a fixed-rate mortgage.

Our specialists will be happy to help you find the right strategy.

-

The SNB policy rate can affect mortgage interest rates. This usually happens quickly with variable models such as the Saron mortgage, as these are based directly on short-term money market rates. Fixed-rate mortgages, however, are driven more by long-term capital market interest rates (swap rates) which to some extent already take into account anticipated future monetary policy and inflation. If a policy rate change is expected by the markets, its effect on fixed-rate mortgages could in many cases already be reflected in the interest rates beforehand.

-

Choosing the term is a strategic decision. Long terms (7–10 years or more) provide you with interest rate security over a long period of time, but are often slightly more expensive. Shorter terms (2–5 years) are usually cheaper, but require you to address the interest rate situation again sooner. Splitting is a popular strategy: you can split your mortgage into several tranches with different terms if required. This spreads the interest rate risk and avoids having to renew the total amount at once at potentially unfavourable conditions.

-

We expect financing costs for both Saron and fixed-rate mortgages to rise slightly.

-

The right mortgage for you depends greatly on your personal risk appetite, your financial situation and your individual needs. Our specialists will be happy to help you find the right strategy for you.

-

Our interest rate forecasts are produced by our economists on the basis of in-depth analyses of the global and national economic situation, inflation trends and the monetary policy of central banks. They represent a likely development. However, ongoing or unforeseen economic or political events can have an impact on interest rate developments at any time. Forecasts should therefore always be seen as a guide and not a guarantee.

-

Prices are mainly influenced by supply and demand. Low mortgage interest rates can generally boost demand for home ownership, as financing costs fall. This can lead to stable or rising real estate prices. Conversely, if interest rates rise sharply, this can dampen demand – but it doesn’t have to, especially if supply remains tight. Political decisions on mortgage lending can also influence demand for residential property and therefore property prices.

-

Yes, that is possible. With a forward mortgage, you can secure the current interest rates today – even if your existing mortgage is not set to expire for several months (e.g. in six, 12 or up to 18 months). Depending on the lead time, requested term and market situation, an interest rate premium (forward premium) may be incurred. In return you will be protected against any interest rate rises until your current mortgage expires. Please contact us for a non-binding quotation.

This document and the information and statements it contains are for information purposes only and do not constitute either an invitation to tender, a solicitation, an offer or a recommendation to buy the related products. The customer or third parties are responsible for their own actions and bear sole responsibility for compliance with legal and regulatory provisions and guidelines. PostFinance has used sources considered reliable and credible. However, PostFinance cannot guarantee that this information is correct, accurate, reliable, up to date or complete and excludes any liability to the extent permitted by law. Information on interest rates and prices is up to date, but the actual development may deviate from these forecasts at any time. The content of this document is based on various assumptions. This means that the information and opinions are not a fixed basis for your financing decision. We recommend consulting an expert before making decisions.

Full or partial reproduction is not permitted without the prior written consent of PostFinance.

Interest rate forecast for download

-

Interest rate forecast for PostFinance mortgages, june 2026 (PDF) The link will open in a new window

-

Interest rate forecast for PostFinance mortgages, march 2026 (PDF) The link will open in a new window

-

Interest rate forecast for PostFinance mortgages, december 2025 (PDF) The link will open in a new window

-

Interest rate forecast for PostFinance mortgages, september 2025 (PDF) The link will open in a new window